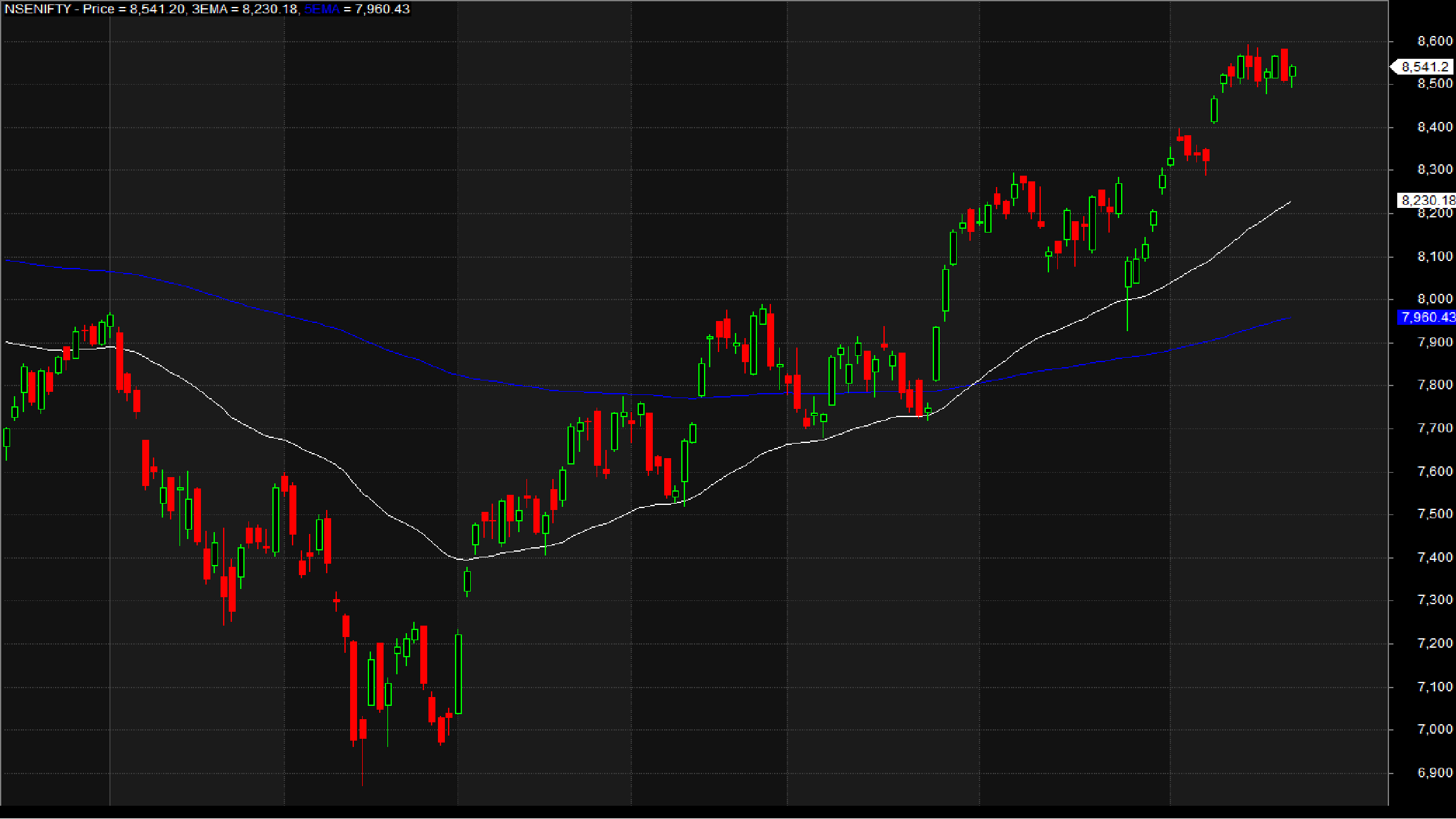

Here’s how it appears when applied on a chart:

Step 3: Evaluating Your Algorithm Through Backtesting

Backtesting is the process of assessing your Algorithm’s performance using historical data. This step is akin to what you manually did in Step 1. Fortunately, Amibroker boasts a robust backtest engine that can complete this task within seconds. All you need to do is import historical data for your preferred stocks into Amibroker. To gain a comprehensive understanding of the backtesting process within Amibroker, please refer to the official documentation link provided below.

Learn more about Backtesting your Trading ideas in Amibroker.

For the purpose of backtesting this EMA Crossover strategy, we’ll use NSE Nifty as our preferred stock, commencing with an initial capital of 200,000 Rupees. Let’s assume that we purchase 2 lots (150 units) per transaction. Upon completing this backtest, you’ll receive a detailed report that includes key metrics such as your Annual CAGR, Drawdown, Net Profit/Loss percentage, and more. You can delve into various parameters by exploring the Amibroker Backtest report here.

Here’s a summary of our initial backtest:

| Parameter | Value |

| Nifty | |

| Initial Capital | 200,000 |

| Final Capital | 1,037,655 |

| Backtest Period | 26-Mar-2002 to 23-July-2016 |

| Net Profit % | 418.83% |

| Annual Return % | 10.45% |

| Number of Trades | 11 |

| Winning Trade % | 54.55% |

| Average Holding Period | 227.91 days |

| Max Consecutive Losses | 2 |

| Max System % Drawdown | -33.24% |

| Max Trade % Drawdown | -29.94% |

While this performance is decent, there’s room for improvement. The drawdown is slightly on the higher side, which could pose challenges for retail investors.

To continue reading this article, please follow this link.

12 Comments