AFL Screenshot

View the screenshot of the McGinley Dynamic Trading System for NSE Nifty below:

McGinley Dynamic Trading System – Backtest Report

This strategy has shown a respectable Compound Annual Growth Rate (CAGR) over the last 12 years, albeit with a slightly higher drawdown typical of trend-following strategies.

| Parameter | Value |

| NSE Nifty | |

| Initial Capital | 200000 |

| Final Capital | 1973764.04 |

| Scrip Name | NSE Nifty |

| Backtest Period | 01-Jan-2004 to 19-Oct-2016 |

| Timeframe | Daily |

| Net Profit % | 771.55% |

| Annual Return % | 18.42% |

| Number of Trades | 128 |

| Winning Trade % | 36.72% |

| Average holding Period | 23.43 periods |

| Max consecutive losses | 9 |

| Max system % drawdown | -17.90% |

| Max Trade % drawdown | -70.97% |

For a detailed backtest report, download it here.

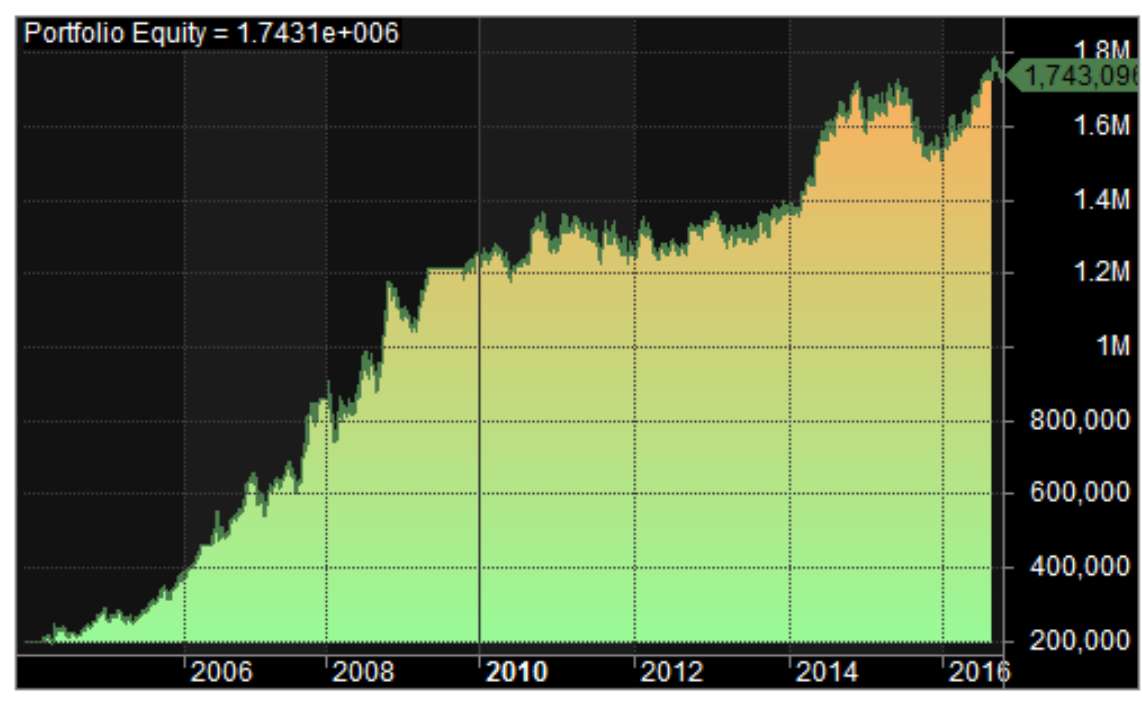

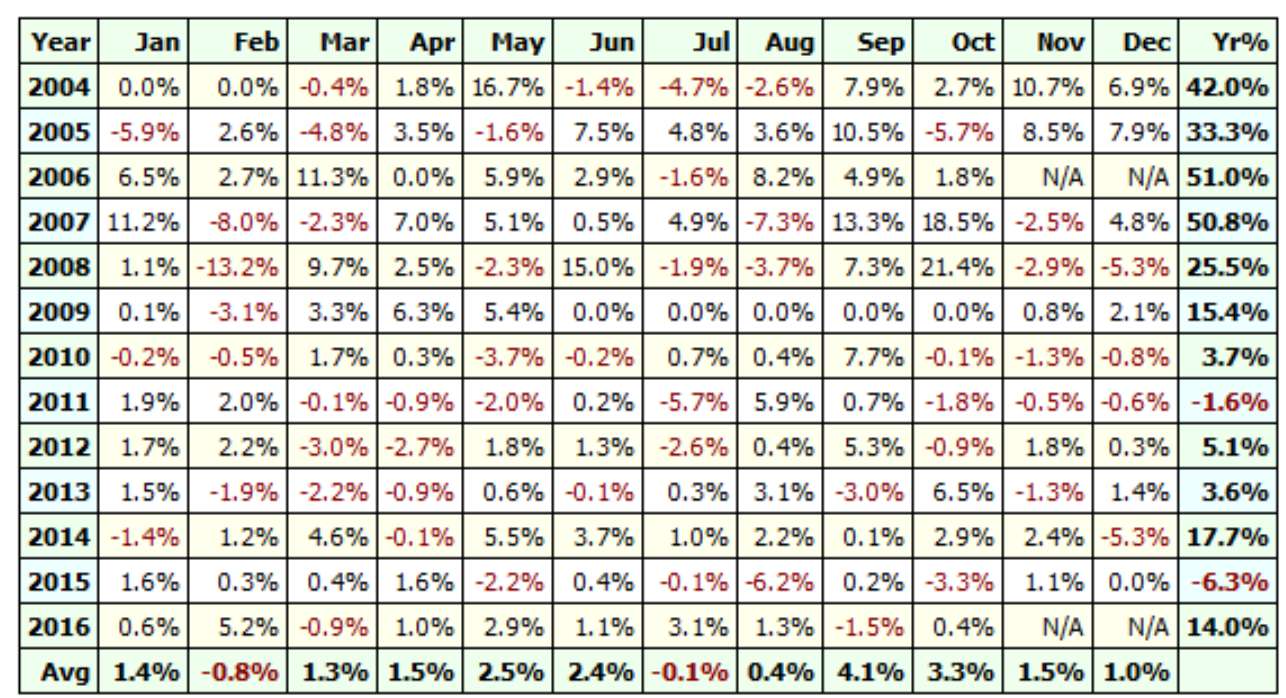

Equity Curve and Profit Table

Explore the equity curve and profit table for the McGinley Dynamic Trading System:

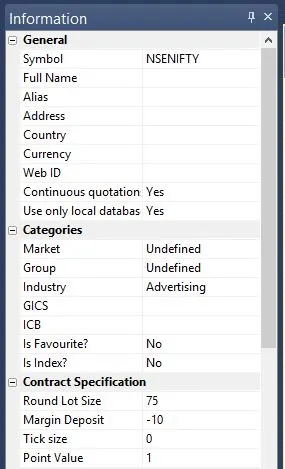

Additional Amibroker Settings for Backtesting

To optimize your backtesting in Amibroker, visit Symbol–>Information, and specify the lot size and margin requirement. The screenshot below illustrates a lot size of 75 and a margin requirement of 10% for NSE Nifty:

One Comment