Time Weighted Average Price (TWAP) is a variation of the Volume Weighted Average Price (VWAP) primarily utilized by large institutional investors to manage substantial orders without causing market disturbances. TWAP represents the average stock price over a specific time period and sets itself apart from VWAP by excluding volume considerations. In this article, we will demystify the process of calculating TWAP and explore its practical applications in trading, including the availability of a TWAP AFL and an Excel sheet.

How to Calculate TWAP?

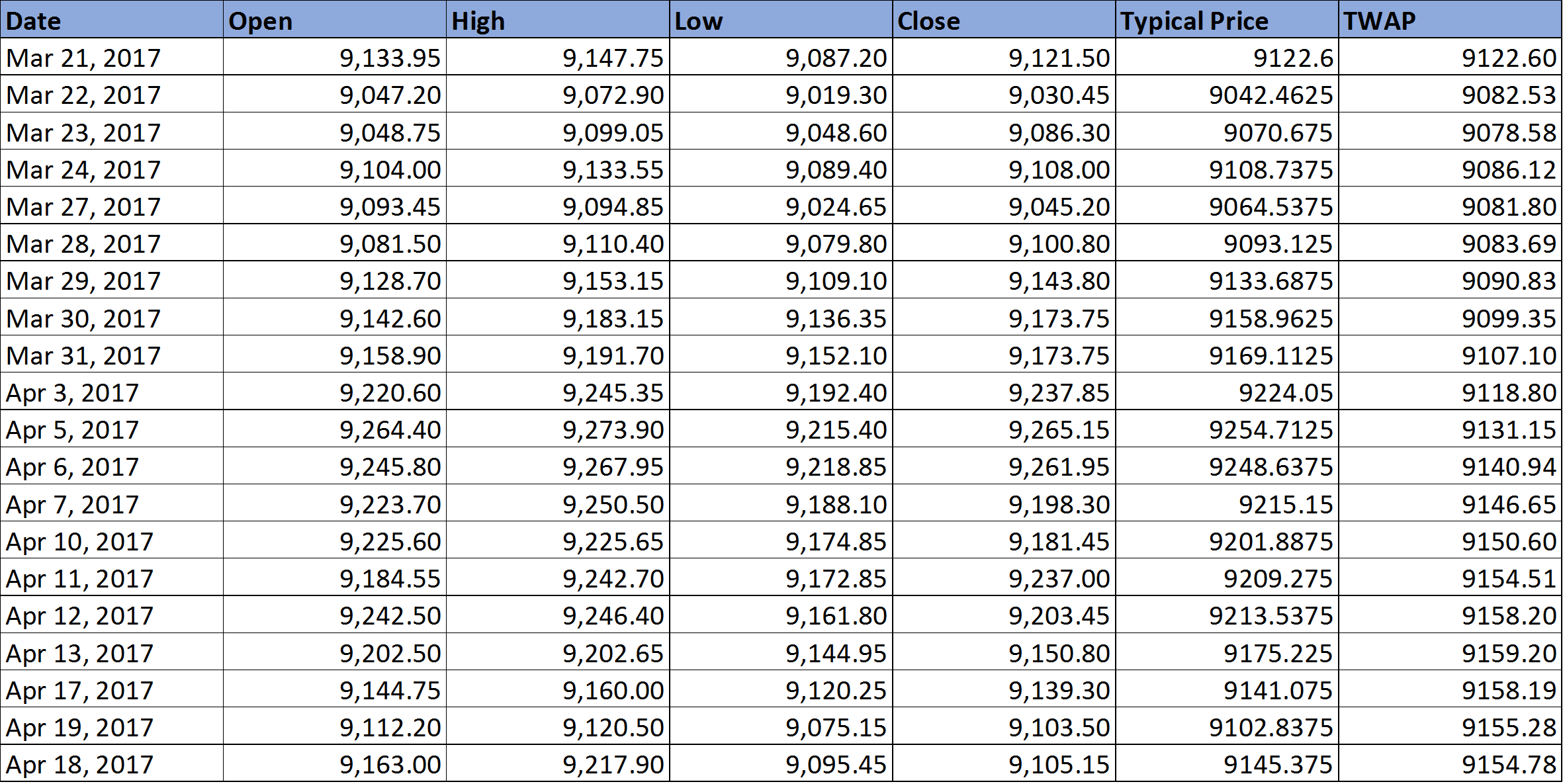

Calculating Time Weighted Average Price (TWAP) is straightforward and relies on finding the average of Open, High, Low, and Close prices for each bar. Here’s a simple example for a 10-period TWAP:

- Calculate the average of Open, High, Low, and Close values for each of the 10 bars (a1, a2, a3, etc.).

- Compute the overall average from a1 to a10: TWAP = (a1 + a2 + a3 + … + a10) / 10.

Notably, the calculation of TWAP doesn’t involve complex mathematical equations, making it simpler compared to VWAP. To assist you further, refer to the screenshot below, illustrating the step-by-step process:

For your convenience, you can download the Excel sheet from the following link:

Using TWAP AFL

Below, you’ll find the TWAP AFL code from WiseStockTrader. While initially designed for intraday trading, this AFL can be adapted for daily or weekly timeframes.