AFL Screenshot

The AFL screenshot depicts Buy and Sell signals using up and down arrows, respectively. A blue up triangle represents Scale-In, while a blue down triangle signifies Scale-Out.

Witness how the position gradually increases for profitable trades:

Observe the gradual decrease in position size for loss-making trades:

Backtest Report

Here’s the backtest report for this strategy. Note that the back tester treats trades involving scaling in or out as a SINGLE trade, resulting in a single row in the trade list. The key difference from regular trades is that it calculates average entry and exit prices based on all partial entries and exits, displaying these averages in the respective fields. Commissions are correctly applied to each (partial) entry or exit based on the partial buy/sell size. To delve deeper into the details of scaling, run the backtest in “DETAIL LOG” mode to observe how scaling-in and scaling-out work, along with the calculation of average prices.

| Parameter | Value |

| NSE Nifty | |

| Initial Capital | 100,000 |

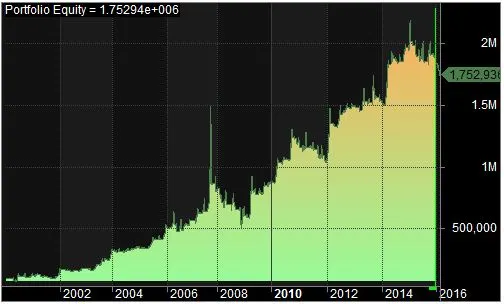

| Final Capital | 1,752,936.03 |

| Backtest Period | 11-Apr-2000 to 23-Feb-2016 |

| Timeframe | Daily |

| Net Profit % | 1652.94% |

| Annual Return % | 19.39% |

| Number of Trades | 146 |

| Winning Trade % | 43.56% |

| Average Holding Period | 14.89 periods |

| Max Consecutive Losses | 8 |

| Max System % Drawdown | -65.87% |

| Max Trade % Drawdown | -85.83% |

You can download the detailed backtest report here.

Please note that even better results can be expected if you allow compounding of your returns.

Equity Curve

Additional Amibroker Settings for Backtesting

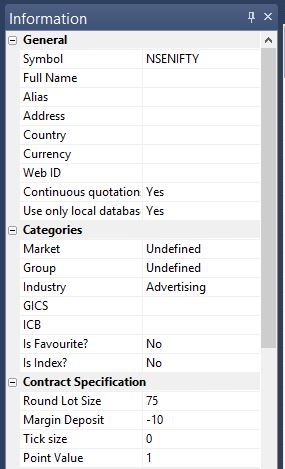

To specify the lot size and margin requirement, go to Symbol → Information. The screenshot below shows a lot size of 75 and a margin requirement of 10% for NSE Nifty: