AFL Screenshot

RMO Trading System- Backtest Report

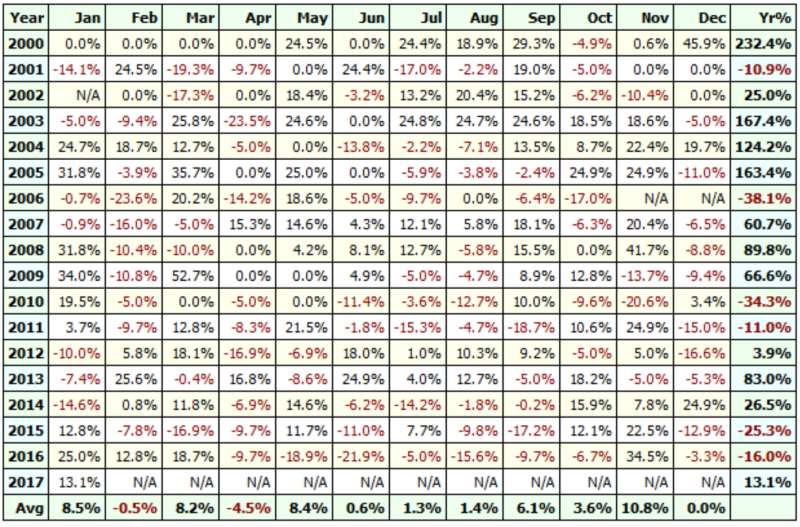

The RMO Trading system has shown remarkable profitability over the last 16 years. However, it’s important to note that the system also experiences significant drawdowns. For an inexperienced trader, dealing with 11 consecutive losses and a success ratio of less than 30% can be challenging.

| Parameter | Value |

| Nifty | |

| Initial Capital | 200,000 |

| Final Capital | 36,656,201.64 |

| Scrip Name | NSE Nifty |

| Backtest Period | 30-May-2000 to 12-Jan-2017 |

| Timeframe | Daily |

| Net Profit % | 18,228.10% |

| Annual Return % | 35.78% |

| Number of Trades | 335 |

| Winning Trade % | 29.25% |

| Average Holding Period | 5.32 periods |

| Max Consecutive Losses | 11 |

| Max System % Drawdown | -70.78% |

| Max Trade % Drawdown | -39.33% |

Download the detailed backtest report here.

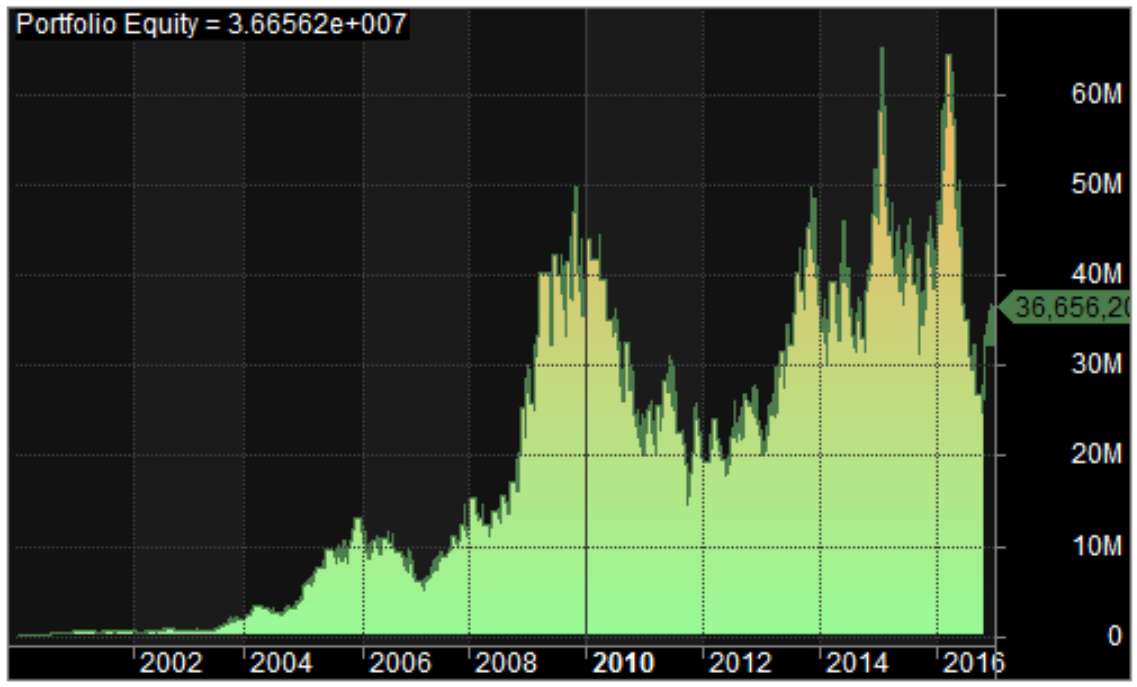

Equity Curve

The equity curve exhibits periods of significant drawdown, indicating its rough nature. Nevertheless, the system maintains overall profitability.

Profit Table

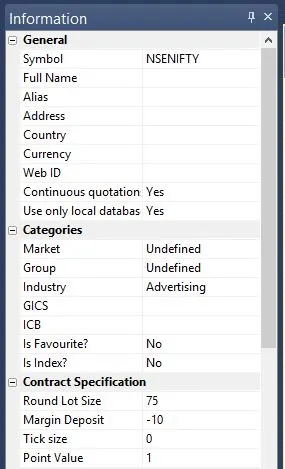

Additional Amibroker Settings for Backtesting

Go to Symbol –> Information and specify the lot size and margin requirement. The below screenshot illustrates a lot size of 75 and a margin requirement of 10% for NSE Nifty:

One Comment